A Timelapse of the Tech Sector, Part 2: After the Internet

/Updated on August 4, 2021

This version has been updated with more sources and source links, more recent data, minor corrections, and more ongoing trends.

Technology as a Cyber Space

After the Internet, changes in technology were primarily digital. While computers kept getting smaller, the main focus became how these computers connect with each other. Technology became more connected, more mobile, and more interactive. The physical components of a computer still had a place in the market, but they were overshadowed by the exponential growth in data. The most valuable technology was used for collecting data, analyzing data, and using data.

The emergence of technology “platforms” defines this new world. At the end of the PC revolution, the IBM PC and its PC clones were the standard for computer hardware, but it was the Microsoft operating systems that became the platform for this standard. Almost every company that made computer programs had to work with Microsoft Windows.

Microsoft was the new IBM.

The Dot-Com Boom (1990s)

In the mid-1990s, when Bill Gates was asked about the biggest threat to Microsoft, he had no doubt. It was the Internet. Microsoft’s operating system risked becoming the same type of generic box that had fractured the PC market. Microsoft owned the market for computer operating systems, but a new layer was forming. The Internet had a different set of standards than individual computers. Inside the Internet, a computer could use programs that run through a web browser. Just like the operating system is the link between a computer’s hardware and the computer’s programs, the web browser is the link between the computer and the Internet. The layers of this market, in a very simplified form, were adjusted for the Internet.[1]

At the bottom layer of Internet software, Microsoft controlled the market for operating systems.

The middle layer of Internet software is the web browsers that linked computers to the Internet.

The top layer of Internet software includes websites and Internet services.

If everything happens online, then the operating system is only useful for making the connection possible. Computer programs would be designed for the web browser, not for the operating system. The type of operating system would no longer have any special value. Internet connection speeds would limit which programs could be used online, but as Internet speeds continued to get faster, maybe Microsoft’s operating system wouldn’t be needed at all. Maybe the web browser would completely replace the operating system. It was a real and serious threat.

Netscape Communications’ 1995 IPO marked the start of the Dot-Com Boom. When the Internet was opened to consumers in the early 1990s, Netscape Navigator came with it, and it was the first web browser to gain universal acceptance. By 1996, Netscape Navigator had about 80% market share for web browsers.[2] Netscape quickly began developing tools that would displace Microsoft’s position in the operating system market.

In response, Microsoft launched its own web browser. The company named it Internet Explorer and packaged it with every copy of the Windows operating system—for free. Internet Explorer was embedded inside Windows and placed in a location that was slightly easier to access than Netscape Navigator. Microsoft also offered favors to other companies that encouraged the use of Internet Explorer.

This caught the attention of market regulators.

In 1998, Microsoft was accused of abusing its operating system monopoly. Just like the mainframe era, where IBM was investigated for using its control of computer hardware to influence computer software, Microsoft was investigated for using its control of the operating system market to influence the web browser market. [3]

Although Microsoft officially lost the case, the final penalty was insignificant, and Microsoft had already won the browser wars. By the late 1990s, Microsoft had achieved more than 90% market share in operating systems (Windows), office software (Excel and Word), and Internet browsers (Internet Explorer). By 2004, Microsoft had a 95% market share in web browsers. Its position was secured.

Meanwhile, the insides of the Internet were following a familiar pattern: thousands of websites came online offering new ways to use the web. All of them promised to change the world. Almost all of them were too ambitious.

The mania surrounding investments during this time period has been well-covered. Our focus here is on the evolution of the technology business. There are many potential markets to explore, but there is only one market that broadly covers the entire Internet: organizing, presenting, and finding the most useful websites. In other words, web portals and search engines.

In the mid-1990s, there were two primary ways to search through the Internet. One was through what is called a “web portal,” a website full of links to other websites that is collected and curated by hand. The other is called a “web crawler,” an automated system that attempts to catalogue the entire Internet and sort websites based on relevance.

The first popular web portal was made by AOL in the early 90s. It was the way that AOL customers saw the Internet. The first powerful web crawler, Alta Vista, came out in 1995. It was made by DEC (remember them?), and was only intended to be a way for DEC to show off its powerful computer hardware. It was not aggressively marketed or supported. Yahoo’s web portal (as yahoo.com) also came online in 1995.

Market share data for these websites from the 90s is hard to find, but the rankings of the most-visited websites show AOL as the top web portal, with Yahoo a close second, from 1997 through 2000 (Yahoo was widely regarded as the king of web portals). Alta Vista was the king of the web crawlers (now called search engines), throughout the 90s, with close to 20% market share in search by the year 2000. Yahoo’s market share for search engines was roughly 35%, but its search engine was also powered by Alta Vista, making Alta Vista’s total US market share an incredible 55%. The Microsoft Network (MSN), Microsoft’s own attempt at a web portal and search engine, was around 15%. Others, such as WebCrawler, Ask Jeeves, Lycos, and Excite, made up the rest of the market.

And then there was Google.[4]

Google did something different. Officially founded in 1998 by Larry Page and Sergey Brin, two Stanford-trained computer scientists, Google’s search engine used a better method and a more Internet-friendly business model. For search, instead of ranking webpages by the number of words that match the search, Google ranked webpages based on how many other webpages were linked to it. For its business model, at a time when every other search engine was attached to a bloated web portal, Google chose to keep it simple. Google did search. It did not do anything else.

The web portal and search engine combinations dismissed Google’s entry to the market, because their goal was to keep Internet users on their own websites for as long as possible, while Google’s goal was to send users to the most relevant website as fast as possible.[5]

Google easily swept through the market. Alta Vista, the only real competitor, was never adequately supported. It went through several owners before it was eventually sold to Yahoo and shut down for good.[6] Yahoo then sold itself to Verizon. AOL merged with Time Warner, collapsed, went independent, and then it, too, was sold to Verizon. Microsoft rebranded its search engine as Bing, but it was never a leader in this market. Google is now, by far, the most popular search engine in the world, with a 92% market share. Its US market share first passed 50% in 2004.

As an endnote to Microsoft’s struggle with the world after the Dot-Com Boom, Microsoft did eventually lose the web browser wars—to Google. Google introduced the Chrome web browser, a simple, lightweight, and easy to use product, in 2008. It achieved a 50% market share in 2015, and sits at about 65% worldwide market share today.[7] As Bill Gates once feared, there are now computers that can run entirely through web browsers. But they do not seem to threaten Microsoft’s position in the market for operating systems.

{kind=link}

Web 2.0 (2000s to Now)

Web 2.0 is a term that refers to websites that rely on user-generated content. It was the next logical step in the evolution of the Internet. Instead of just looking at websites, individual people could also add their own content. This means home pages, blogs, and videos.

In 1998 and 1999, the top two most visited websites were AOL and Yahoo. The third was GeoCities. GeoCities was a web hosting service that allowed anyone to have their own home page. It was a crude way for individual people to mark their place on the Internet. There was not much interaction between users, but it relied on user-generated content to sustain its popularity—a preview to the next generation of the Internet.

In 1999, GeoCities was purchased by Yahoo. But it was shut down in 2009, shortly after social networking became the new standard for web 2.0. Internet users did not just want to mark their place on the Internet. They also wanted to interact with each other. Message boards and chat rooms had been around for years as a feature of web portals such as AOL and Yahoo, and they had even existed since 1980 as a service called Usenet, but they were not the same thing as interactive home pages. Social networking combined home pages with interaction between users.

A few small failures appeared in the late 90s, but it was the early 2000s that exploded with new social networking platforms (now called social media). Friendster and LinkedIn were founded in 2002. MySpace appeared in 2003. Facebook in 2004. Twitter, 2006.[8] They came with dozens of now-forgotten social networking sites. Each individual social media service was designed for a different type of audience:

Friendster and MySpace for the average teenager.

LinkedIn for professional networking.

Facebook for college students.

Twitter was intended to be a simple text messaging service.

The market share numbers for social media platforms are misleading because each platform serves a different function and many people use multiple platforms. But the number of users represents a good proxy for market share in the age of social media. Friendster peaked at over 100 million users, but it was nearly abandoned by 2004, only two years after its beginning. The website was easily overtaken by MySpace. Friendster limped along for years, and finally shut down in 2019.

MySpace had a more open and adjustable platform, and its webpages loaded much faster. But its position in the market was just as delicate as Friendster. MySpace was purchased by News Corp in 2005, and became the most-visited website in the world the next year. In 2008, MySpace was surpassed by Facebook, just two years after Facebook opened beyond the college demographic. Then the company was sold two more times: to Time Inc. in 2016 and the Meredith Corporation in 2018. It still exists, but it is also nearly abandoned.

Facebook had a more mature way of presenting information than MySpace did. Every Facebook page looked basically the same, and was laid out in a simple, easy-to-understand way. It did not have the painful custom backgrounds and loud music that came with many MySpace pages. Facebook also introduced a new feature called newsfeed, which allowed users to see what their friends were posting without having to stalk their profiles for new information. The combination of these small changes made for a much better experience.

Facebook is now the third most visited website in the world, and has more than 2.8 billion monthly active users. With such a large number of users, it will be very difficult for any other social media service to compete, because a significant part of the value for Facebook’s users is that their friends are already using it.

LinkedIn and Twitter do not directly compete with Facebook. They have carved out their own small pieces of the social media market: Twitter has just more than 350 million monthly active users, while LinkedIn (which was bought by Microsoft in 2016) has about 310 million. There are younger social media websites that have already reached a similar size: Pinterest, which was founded in 2009, has almost 500 million monthly active users, and Snapchat, which was founded in 2011, is near the 300 million user mark.[9] There are also a few massive social media sites based in Asia. But Facebook is the worldwide leader.

Part of Facebook’s influence comes from a relentless urgency to acquire potential competitors. A feature of this new web 2.0 world is that successful startups are bought out by larger companies before they can become a real threat.

YouTube, by far the world’s largest video hosting site (and second most-visited website in the world, behind Google), was founded in 2005. It was bought by Google in 2006.

Instagram (1 billion monthly active users), was founded in 2010 and purchased by Facebook in 2012.

WhatsApp (more than 2 billion monthly active users), was founded in 2009. It was also bought by Facebook, in 2014.

The social media market is nearing maturity. Facebook is still looking to buy anything that comes close to competing. Any social media service that refuses to be bought can expect to be copied.[10]

The Smart Phone Era (2000s to Now)

As computers continued to become smaller and more connected, the natural extension of this process was that more computer components found their way into mobile phones.

The first smart phone, a computer within a mobile phone, was actually developed by IBM, all the back in 1992. It had most of the features of a modern smart phone, but it was too far ahead of its time. The communication networks required to support a smart phone market were too slow and underdeveloped.

The precursor to modern smart phones was the Personal Digital Assistant (PDA). PDAs were tiny computers with a few limited functions that allowed access to Internet and email. They were not phones. The most popular PDA was made by Palm (founded in 1992), which had more than 77% market share by 1999.[11]

In PDAs (and later mobile phones), the market layers are the same as personal computers. Simplified:

The bottom of the market for PDAs (and smart phones) is the hardware layer. This is physical the device.

The top of the market for PDAs (and smart phones) is the software layer. This is what makes the device useful. For this part, we are only interested in the operating system.

In 2000, Palm’s market share had fallen to 72%. In second was Handspring, a PDA device maker founded in 1998 by defectors from Palm. But Handspring was also using the Palm operating system. This meant that Palm’s operating system for PDAs had reached 85% market share. A small portion of the remaining market included some familiar names: HP, Compaq, and Microsoft.

Following the expectations of the patterns from the personal computer revolution, Palm had an enviable position in the market for PDA operating systems. It was almost as powerful as the Microsoft platform, but it could not maintain the standard. By 2001, Palm’s market share for PDA operating systems dropped to about 65%. At the end of 2001, it was about 50%, and it continued to fall.[12]

Like the beginning of the personal computer revolution from the previous decades, most of the production was vertically integrated. Each smart phone or PDA (or “pocket pc” depending on who you asked) was a computer that came with an operating system, and the phone operating systems were almost entirely made by the same company that designed the phone.

Research In Motion (RIM) was the first to master a smart phone design. The company had been around since 1984 and made personal pagers through the 90s, but did not make a real phone until 2002.[13] The company called it the BlackBerry. Fans called it the “crackberry” because of its addictive design. At the time, the mobile phone market was already dominated by the Symbian operating system (developed by Nokia, used by Nokia, Motorola, Sony, Panasonic, and Samsung), which had an 80% market share. [14] The BlackBerry quickly established RIM as a leader in business phones. Within two years, RIM had captured almost 20% of the PDA market.

By 2005, PDAs were fading, and smart phones were the hot new product. The US market for smart phone operating systems was split evenly between four companies, without any clear leader or standard: Symbian, RIM, Palm, and Microsoft (used by Motorola, Palm, and Samsung).

Then Apple surprised the world.

When Steve Jobs introduced Apple’s first smart phone in 2007, he described it as three separate products: “an iPod, a phone, and an internet communicator.”[15] It was a convergence of technology that no other company had achieved, wrapped in a consumer-friendly package that no other company had considered. And, in a parallel to Apple’s choices during the personal computer revolution, it was fully vertically integrated. Apple designed both the phone and the operating system.

Within a year, Apple’s iPhone had reached 10% US market share. In two years, it was up to 20%. By then, Symbian and Palm were almost eliminated. RIM’s dominance continued to grow, while Microsoft continued to fall behind.

But smart phone buyers were increasingly focused on smart phone features, which RIM was neglecting. RIM viewed smart phones as a purely business device, while everyone else believed that smart phones could be useful beyond business. And that’s where the market was growing the most.

Behind this big battle for market share, way under the radar, was Google’s smart phone operating system, called Android. It was announced in 2007 and released in 2008. And as part of Android’s development, Google also led the way in creating the Open Handset Alliance. This was a group of 34 companies involved with every piece of the smart phone market that all agreed to use the same standards—and they would all use the Android operating system. Google had convinced the market to use Android, much like IBM had chosen Microsoft more than 20 years earlier.[16]

With Android, Google was using the same strategy that worked for Microsoft during the personal computer revolution: focus on the software layer and force the smart phone hardware to become generic boxes. If every smart phone app was designed for Android, then smart phone manufacturers would be forced to use it, or they would lose access to those apps. To make their decision easier, Google licensed it for free. The company’s plan was to make money through the advertisements that appear on Google’s apps inside the phone.

Google’s Android was quickly adopted as the standard. It became what Symbian had intended to be. By 2012, it had a 50% global market share. It is now at more than 70%, with Apple taking the rest of the market. After Microsoft gave up on the smart phone market in 2017 (with a 0.1% market share), there is no one else left.

The early leaders in the PDA market were eliminated. Palm sold itself to HP in 2010, and the guts of the company were later split up and sold again. RIM renamed itself BlackBerry. It continues to be an independent company, but no longer has any influence on the smart phone industry. RIM now makes Android phones.

The smart phones, other than Apple’s iPhone, have become generic phone boxes with Android on top, just like PCs are generic computer boxes with Microsoft Windows on top. Motorola’s mobile business was purchased by Google in 2012, broken apart, and resold to Lenovo in 2014. Nokia’s mobile business was purchased by Microsoft in 2014, broken apart, and resold through 2016 and 2017. The comparisons to the PC market are uncomfortably similar.

The competition for what goes inside a smart phone—the bottom layer for smart phone hardware—was just as deep, but not as interesting. The short story is that mobile phones don’t have Intel inside. They did, but not for very long. Qualcomm, using processors designed by ARM, replaced Intel’s standard (ARM only designs processors; it does not manufacture them). Smart phones required a less powerful processor than a full computer, and their design was focused on using less energy (so the battery would last longer). By 2010, ARM had a market share of 95% for mobile phone processors.

The current market is described as a “System on Chip” (SoC), or an entire computer on one small chip, rather than just a processor with other components connected. MediaTek carries a global SoC market share of 37%, while Qualcomm had 31%, with Apple in third at 16%.[17] Many companies in the SoC market rely on ARM-designed processors. The way that this market is measured has changed over time (it can’t be compared to the 2010 number), but ARM’s influence is certainly fading. ARM has been the market leader in the “design” market since the category was created, but it has declined over time, with a current market share of about 40%.

Intel and Microsoft both failed to transfer their PC market power to mobile phone market power, and ARM is currently targeting the personal computer market. Because of the growth in the smart phone market, Intel’s market share in the entire universe of microprocessors (for computers of all sizes) is already down to less than 20%. The competition in microprocessor technology continues to intensify.[18]

The App Revolution (2010s to Now)

In 2009, less than 1% of all web page visits came through a mobile phone. Less than ten years later, that number was already more than 50%, and it continues to stay around 50%.

The trend is even more pronounced within social media networks. In 2013, Facebook already had 68% of the time spent on the network (for US users) coming through a mobile phone. Twitter was even higher, at 86%. And Instagram had an astonishing 98% of its US usage happening on a mobile phone. I could not find more recent data for these individual services, but an updated review of the social media market provides the big picture: 99% of social media users access social media websites from their phone, and 72% of social media users access social media entirely from their phone. Social media has become mobile media.

Smart phones have eliminated the need to say “brb” (that’s “be right back” for anyone who missed the Dot-Com Boom). The phone is always there. At the same time, waiting in line has been replaced by phone entertainment time. Reading the newspaper has become a “reading the phone” activity. Almost anything that can be done online can be done on a phone.

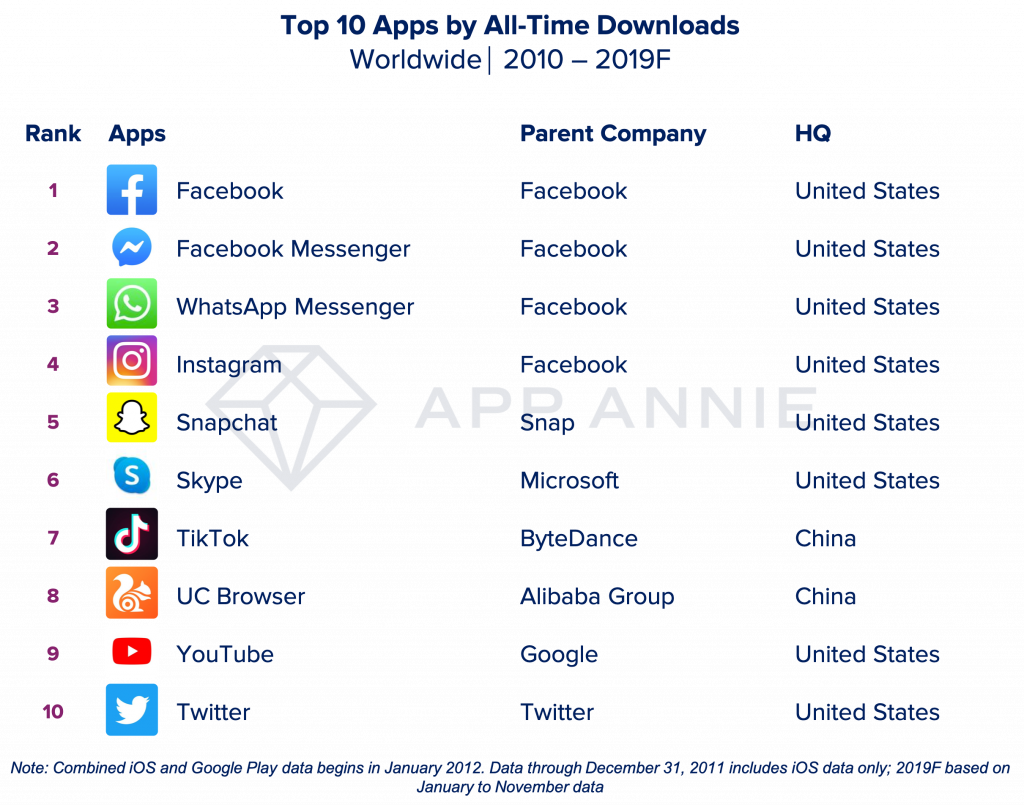

The transformation is still ongoing. The app revolution is near the end of the fluid stages, where thousands of new entries cram into the market, each one promising a market disruption. But the most downloaded phone apps of the 2010s decade include some familiar names:

{kind=link}

Facebook (owned by Facebook)

Facebook Messenger (owned by Facebook)

WhatsApp Messenger (also owned by Facebook)

Instagram (also owned by Facebook!)

Snapchat (independent)

Skype (owned by Microsoft)

TikTok (owned by ByteDance)

UC Browser (owned by Alibaba Group)

YouTube (owned by Google)

Twitter (independent)

All of the top four apps of the decade are owned by Facebook. One is owned by Google. And one is owned by Microsoft. Web 2.0 has shifted to mobile phones. Social media has a natural attraction to technology that is more mobile and more connected. It was a movement that makes it even easier to be online.

If we include the apps that come with an Android phone, Google has 12 of the top 15 installed apps (on android), while Facebook claims the other three. There are questions about which apps are used the most often, and which apps might rise up in the future, but it is undeniable that the Android operating system has ensured Google’s position in the age of the app.

End of Part 2

Part 2 is more complicated than Part 1. It is not just the story of one firm’s influence. The standards for each different market were set by the services that managed to gain the widest adoption. At first, this was determined by which ones were the easiest to learn and the most useful. Google’s website was as small as possible. Just type in what you want to find. Apple’s iPhone was a milestone in simplicity. Anyone could learn how to use it. Facebook’s design was easy to navigate. It gave users the information they wanted without the clutter of endless customization. Google’s Chrome browser also followed this theme.

Over time, the services that became dominant were the platforms that had already reached a critical point of acceptance. Google’s Android phone operating system replicated the success of Microsoft’s Windows by starting as the standard platform. If anyone wanted to replace Android, then they would also have to replace all of the apps that were made for Android—and this is not possible.

The market leaders in one age do not always dominate the next. IBM, Intel, and Microsoft all missed the move to mobile phones (this does not mean they became irrelevant, only that they missed the new market). Even Palm and Nokia were unable to translate their early success into what Apple and Android ultimately became. These positions are very hard to defend or expand, and they can disappear in an instant.

But can these major market changes be predicted? That is the question everyone wants to know.

Andrew Wagner

Chief Investment Officer

Wagner Road Capital Management

[1] There are many other layers involved with Internet connections, but the market for web browsers provides the most instructive story.

[2] From The Motley Fool.

[3] CNET has a good summary of the case against Microsoft and how it compares to IBM’s antitrust lawsuit. John Borland’s article for ZDNet also summarized the browser wars.

[4] A short history of Google can be found on searchenginehistory.com.

[5] Web portals and search engines both made money by selling advertising space on their pages. The value of that advertising space was roughly determined by how many people visit the page and how many people click on the advertisements. The primary advantage in business strategy is that Google was better at showing people the advertisements that they wanted to see, just like it was better at showing people the websites that they wanted to find.

[6] A sad summary of AltaVista’s potential is covered by Claire Broadley at Digital.com.

[7] A previous version incorrectly stated higher market share numbers. This has version has been corrected with more accurate data.

[8] When these social media companies were founded, their peak sizes, and what happened to them is all summarized in an article by Matthew Jones for the History Cooperative.

[9] Snapchat’s active user count is measured in daily active users.

[10] Facebook’s defense of its market is remarkably similar to the ambition that drove Microsoft throughout the 90s. This behavior, like Microsoft’s, has attracted the attention of antitrust regulators.

[11] The story of Palm is summarized in a Fast Company article by David Lidsky.

[12] These numbers have slight differences depending on the source, but this version has been updated to reflect the best known numbers. The rapid decline in Palm’s market share is consistently reported from 2000 to 2010.

[13] A short history of RIM can be found in an article in The Canadian Encyclopedia by Iris Leung.

[14] The Economist wrote a special report on this market back in 2002, speculating that Nokia would most likely be the winner.

[15] Apple’s iPhone announcement is still available to watch on YouTube.

[16] The Open Handset Alliance now has 84 member companies.

[17] All Apple SoC are used in Apple phones.

[18] An equally intense battle is happening in the market for graphics processors, which are used for more complex operations that are vital for most of our future themes. But those themes are coming later in the next part.

Marketing Disclosure: Wagner Road Capital Management is a registered investment adviser. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and, unless otherwise stated, are not guaranteed. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed herein. Past performance is not indicative of future performance.