A Timelapse of the Tech Sector, Part 3: The Future of Tech

/Updated on August 4, 2021

This version has been updated with more sources and source links, more recent data, minor corrections, and more ongoing trends.

The Future of Tech

The future of tech will be driven primarily by two major themes. Both are a continuation of decades-long trends:

Faster Internet connection speeds will enable more devices to come online and create a more decentralized network.

Faster, smarter, more efficient components will continue to make computers more powerful and more interactive.

How these trends affect individual markets is nearly impossible to predict, but most of them follow a familiar pattern. Every new technology goes through series of waves. A summary of this process happens in about four or five stages.

A new technology becomes viable, introducing hundreds or thousands of startups trying to capture a piece of the new industry.

The businesses with the best combination of technology, attractiveness, and strategy become stronger.

The weaker businesses start dropping out of the market.

Consolidation begins. Stronger businesses buy out what remains.

The market matures. In most cases, this leaves only 3-5 businesses that still have the ability to compete.

Predicting stage one is the hardest. At that stage, the best evaluation comes down to who has the best ideas or the best technology. Picking the right one is not much better than choosing the right lottery number—low chances, but extraordinarily high payout.

From there, it gets less rewarding, but easier to see. When the weaker businesses start to fall behind is probably the optimal time to consider investing—there is much more certainty, but still significant upside. By the time the market matures, the remaining companies often begin to pay out healthy dividends, because they don’t have anything else to do with their money—their position is already secured.

We can’t say for sure which companies will win their market wars, because the one with the best technology is not always the one with the best business. But we can evaluate where everything stands at the moment, consider the historical context, and try to match it to the future.

Ongoing Trends

When we talk about the future of tech, we’re only looking at what is just now starting to gain momentum, and we’re not making any bold predictions about what might come next. Most of these big ideas are already old news for the people paying close attention—and the biggest names in tech are already making substantial investments in every one of these areas—but their rise to prominence is only within the past five years. I can’t predict which one will become the most important, but this is what I perceive to be the most developed markets (I can’t tell you what I’m finding, but I can tell you where I’m looking). They are all enabled and facilitated by the two major themes mentioned above.

Cloud Computing

Mainframes never completely disappeared. They’re still around, and they’re still mostly made by IBM. These mainframes serve as a secure backbone for mobile apps that require encryption, such as credit card transactions. But software that doesn’t need as much security is moving to the “cloud.” The cloud is a network of large computers, called servers, which function like mainframes. What this means is that computer programs no longer need to run on your computer—like the mainframes of the past, a big machine can do all of the work while the smaller ones ask for the answers. This has enabled businesses to begin offering software that can be rented for a monthly fee (called “Software as a Service,” or SaaS) instead of software that you can buy and own forever with one payment.

The origin of SaaS applications actually goes all the way back to the 1960s, in the form of “time-sharing” on mainframe computers. As we described in Part 1, when computers became smaller and more powerful, they could do more of the work on their own without the help of a larger computer. SaaS fell to the background until the introduction of the Internet created more opportunities. As network speeds increased and more devices came online, SaaS applications have become pervasive, especially in the past five years.

There are thousands of specialized SaaS companies, covering everything from movies and music to accounting and HR, but the cloud computing background (sometimes called Infrastructure as a Service, or IaaS) is dominated by some familiar names. Amazon jumped into the business before most people knew it existed, and remains, by far, the leader in cloud systems, with a 41% market share. Microsoft is a distant second, with 20% market share. Google is even farther behind, with a 6% market share. Even with no market share changes, the tremendous growth of this market will benefit every major player: The worldwide IaaS cloud computing market grew by 40% in 2020.[1] This segment of the market is already well-established, but still fast-growing.

Despite such fast growth, I consider the IaaS part of cloud computing to be the most developed market among these ongoing trends, because it requires immense investment to break into and is already under control by the firms that have the funds to make these massive investments. But there are many other SaaS opportunities.

The Internet of Things (IoT)

IoT is self-descriptive. It refers to the ability of any object to be computerized and connected to the Internet, a direct result of the computer technology that continues to get smaller. The most well-known advancement in this area includes “wearable devices” such as smart watches and “smart home” devices that respond when you talk to them. But it opens up other possibilities as well, such as self-driving cars and high quality medical monitoring devices.

There is not much to say about IoT. In the market for self-driving cars, Google’s Waymo is the industry leader in an industry that does not yet exist. In the market for “smart speaker” home assistants, Amazon (Alexa) is the current market leader in the US, with an installed base of 53%, while Google (Google Home) has 31%. There are no other significant players in that market. Apple is currently the worldwide leader in smartwatches, controlling about half of the market with no serious competitors.

Any assessment of IoT must consider the companies producing the hardware that goes inside Internet devices (who is making the microchips?). While the big players are competing with each other, they often share the same suppliers. The result may be that investing at the hardware level will achieve better returns than looking at the top, but the financial stability for suppliers is generally more uncertain.

Artificial Intelligence (AI)

AI is an attempt to get computers to be good at things that humans are good at. Computers are already very good at analyzing data, especially large sets of data, but they’re not as good at things that require more intuition, such as medical diagnosis and speaking. AI technology is already starting to replace specific jobs done by accountants and lawyers, and has the potential to start affecting the medical field. It also has a promising potential for enabling self-driving vehicles.

AI is a very competitive technology. Almost every software company is making some type of investment in this space, and this includes the big ones: IBM, Google, and Microsoft are all boasting about their AI capabilities. There is very little opportunity for direct investment in this field. It is generally a small piece among many other projects, but companies focused on specific AI applications are worthy of investigation.

Blockchain

For the past ten years, blockchain has been one of the most popular topics among tech enthusiasts. It only became a mainstream phenomenon within the past five years, when investment became easy and financial publications began tracking the price of cryptocurrencies in real time.

The basic idea behind blockchain is called a distributed ledger. The ledger part means exactly what it sounds like—a record of transactions. A distributed ledger is one that keeps a record of transactions in many different places simultaneously (instead of a centralized ledger, like a bank’s records). I won’t get into the details of how this works. The most important thing to be aware of is that blockchain can do some things well (tracking transactions), and other things not as well (it’s slower than centralized ledgers).

There are thousands of cryptocurrencies in the market, each one claiming to solve a different problem, all of them promising to change the world. Most of them cannot do what they claim, and almost all of them will fail. The easy money in this market has already been made—cryptocoins are treated like commodities, and the early traders have already captured most of the big moves.

The future of blockchain is not investing in cryptocurrencies. Like the promise of the Internet, the most valuable part of the blockchain technology will come from how non-tech businesses use the technology. For example, major companies are currently exploring how to use blockchain to track and manage their products. It’s not a disruptive threat. It’s a business tool.

Quantum Computing

Moore’s Law has reached its ceiling. The laws of physics prevent microchips from packing in any more transistors. The next step in the process could be a quantum leap. Just like the switch from vacuum tubes to transistors, and transistors to microchips, the introduction of quantum computing has the potential to replace the previous generation. But right now it’s just potential. The cost of producing these systems, the complexity of their operation, and the physical size of their hardware, are all reminders of the mainframe era.

Quantum Computing is a significant area of interest for IBM, Google, Microsoft, and Intel, but Google is currently producing the most powerful quantum computers that are not created by a government entity.

5G

Internet speeds and connections have become more complex and more widely used. This is where 5G comes in, as the next revolution in the process. Mobile phone networks currently use primarily 4G technologies, and 5G is more than 10 times faster, fast enough to rival the speed of home Internet connections. The buildout of this new 5G network is certainly a major investment opportunity, but what it enables (more data transmission) will have an even larger impact. It makes cloud computing more valuable and it makes IoT and AI more capable.

Excellent 5G investments can come from many sources. A few of them to consider could be network security companies, network infrastructure testing and building, device hardware and security, or any of the technologies that are enabled by 5G.

Virtual Reality (VR) and Cybernetics

Computing devices have become easier to use over time as the interaction between the device and the user becomes more intuitive. VR is just an extension of this long-term trend. Right now, VR is limited to creating a more immersive entertainment or educational experience than TV screens. The most common use comes in the form of video games. Whether this technology will become widely adopted is still unclear. It is too early to tell.

Cybernetics is an even bigger extension of this trend. Instead of having a virtual reality device that you wear on your face, cybernetic technologies introduce the idea of creating an entirely new robotic eye (or arm, or leg, or anything). This is when the device becomes part of the person, and this is where technology is going. But it will be a few years before we get there, and “bio” tech is outside the scope of this overview.

Conclusions

Anyone who follows the technology sector knows that I left out some very important features. It’s not possible to cover everything, but it’s also important to be aware of what I missed.

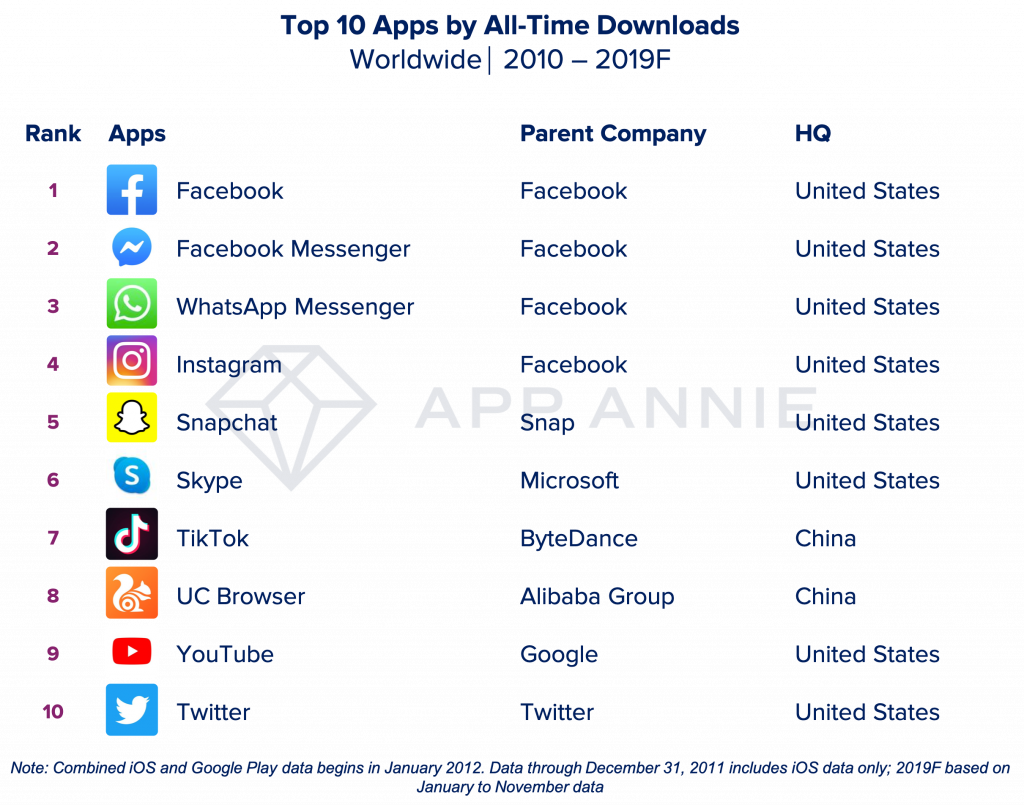

The rise of the Asian giants is the biggest hole in the story. From Part 2, if we review the top 10 most downloaded apps of the 2010 decade, two of them, TikTok and UC Browser, are owned by Chinese companies. In 2020, the most downloaded app in the world, TikTok, came from China. And while Chinese-owned apps are unlikely to be direct competitors to Western Internet companies, it is a transformation worth watching. Intel’s decision to switch from memory chips to microprocessors was also triggered by the advance of Asian memory chip manufacturers. All of these apps are running on Google’s Android or Apple’s iPhone, but a Chinese competitor, supported by the Chinese government, could still join the market. The Chinese government also boasts the most powerful quantum computer, and Chinese technology firms are formidable global competitors. Most of the worldwide discussion has been about Western firms penetrating the Asian market, but it’s worthwhile to consider the opposite possibility. [2]

{kind=link}

There is another general theme that must be addressed: why do some technologies and companies find success, while other flame out? There have been hundreds of books written about this question. For technology, based on the background sources of my review here, there are a few common traits.

Sleek and simple designs do best. Big and bloated (and confusing) will eventually be eliminated. Apple was the original master of this ideal for hardware. Google’s website brought it to the Internet. Facebook’s design took it to social media. These are not products that are just better technology, they are also more convenient and easier to use.

The connection between different layers of the market affects which technologies become the standards. Historically, hardware quickly becomes a group of generic boxes, while the software on top sets the standard. However, sometimes hardware inside the system also becomes a standard. For example, Corning has been the main supplier for the glass on Apple’s iPhones since the very beginning. Also, from this report, Intel’s computer processors and ARM’s phone processors showed a similar dominance as essential pieces of their device’s hardware. There is more than one place to look.

A bad strategy and an arrogant management were universal predictors of a failure to adapt. The pattern for failure is consistent: dismiss a competitor’s major announcement, ignore their success, and then follow them into the market (much too late). It is always far better to be proactive rather than reactive. Technology moves too fast to wait for competitors to think of the next best idea. The side note to this observation is that this pattern for failure often started after the founder left the company: From the PC Revolution, Commodore and Compaq both went down after the founder’s departure. Apple, Microsoft, and even Dell struggled when the founder left (all three managed to survive and thrive, but briefly lost their touch for innovation). In other words, it’s not just about products. It’s also about plans.

There were also many dead-end designs that I did not discuss, and some missed opportunities that I left out of the story. It’s easy to look at the businesses that still survive and see that their success was obvious. In most cases, it was not obvious. The best product was not always the best seller. It is also true that the companies that fail to become the standard for one market do not necessarily die. They often have other lines of business where their approaches were more successful. The real test is one of purpose. Was the company’s new product only made as a response to competitors, or is it genuinely providing a better customer experience? The customer-focused firms tend to find more success, while the followers continue to fall behind.

But the move to another market can also be tricky. There is one familiar feature of today’s market structure—regulatory risks. As IBM learned in the 70s, and Microsoft re-learned in the 90s, industry regulators do not like it when a company uses its high market share in one market to try and eliminate potential competitors building alternative platforms. The antitrust suits against those two companies were distractions at best, but possibly crippling. Fear of regulation can slow a company’s innovation, but the reality of regulation can break it apart.[3] Over the past 2 years (major antitrust investigations seem to have a 20-year cycle), Facebook, Google, and Amazon have all been sued for antitrust law violations. These lawsuits are still in various stages, and we will see how they affect these companies.

Beyond markets, there is one more topic that I consistently avoided—stock prices (and financial returns). The story here emphasizes the creative destruction process without mentioning the prices paid for acquisitions or the stock prices of the public companies. If those were included, it would show that the initial buyers almost always paid too much for their growth opportunities, while businesses that kept trading owners were almost always dramatically losing their value over time. And the investors in public companies were routinely over-estimating a company’s growth. You can be right and still pay the wrong price.

The final conclusion comes from two important questions: Why go so far back in history? And does this give us any special insights for future investment ideas?

The answer to both of these questions is the same. To repeat our description from introduction: “What it reveals is a pattern that may be useful for future long-term predictions. It can also translate into a general understanding of how markets can become fragmented with every new innovation, mature over time, and consolidate into a small number of major winners.”

As for the future of tech, it’s hard to predict who will win this round. If it’s a startup, it will be one that competes by avoiding the bigger players, like DEC and Compaq in the past. If it’s a larger company, it will be one that persuades the others to use its technology as the standard, like Intel, Microsoft, Google, and ARM. But whoever leads the transition into the next stage of computer technology is not destined to remain the leader forever. In fact, history would advise against betting on the early leader. Then again, history would also advise against waiting too long to make an investment, because the one that wins tends to win big, with a market share that can surpass 90%, and investment returns that outperform for decades at a time.

That’s why we do the research.

Andrew Wagner

Chief Investment Officer

Wagner Road Capital Management

[1] IaaS market share numbers and industry growth come from Gartner.

[2] One issue that I did not have space to address is the substantial investments made by governments that provided the basic research needed for new technologies. A company can plan for research that takes 5 to 10 years to reach the market, but a government has the resources to take on major projects with timelines of 30 years or more. An amazing example is ARPANET. This project, paid for by government contracts, proved that networking was possible and accelerated the introduction of the Internet. An excellent book about this topic is Where Wizards Stay Up Late by Katie Hafner and Matthew Lyon.

[3] For example, Bill Gates blames the antitrust distraction on Microsoft’s failure to move into mobile phones, and IBM considered antitrust issues when it entered the personal computer market.

Marketing Disclosure: Wagner Road Capital Management is a registered investment adviser. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and, unless otherwise stated, are not guaranteed. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed herein. Past performance is not indicative of future performance.